Executive Summary

- Total home sales in the greater central Los Angeles area were 2 percent below last May, following April’s upwardly revised 2 percent year-over-year increase.

• Sales between $2 million and $3 million saw a 6 percent jump compared to last May, the first year-over-year increase following six months of double-digit declines, driven by East Valley, Eastern Cities (Arcadia and Monrovia), and Foothill Communities.

• Home sales activity remains relatively stronger on the eastern side of Los Angeles and among homes priced below $1 million – including Eastern Cities, Foothill Communities (La Cañada Flintridge, La Crescenta – Montrose), East Valley (from Sherman Oaks to Glendale), and also South Bay.

- For-sale inventory is up 10 percent year-over-year, a notable slowing from 20 to 30 percent increases seen during winter months.

• Relatively larger for-sale inventory growth is seen in western parts of Los Angeles, including Mid City, Sunset East, Silicon Beach, and Brentwood, while inventory is aging without an increase in new listings on the East Side, NELA, North Valley, and areas surrounding DTLA – days on market has increased relatively more, up 17 days YOY.

- While demand for homes priced below $1 million remains solid, buyers are taking longer to make the purchase leading to longer days on market, up 7 days YOY to an average of 27 days.

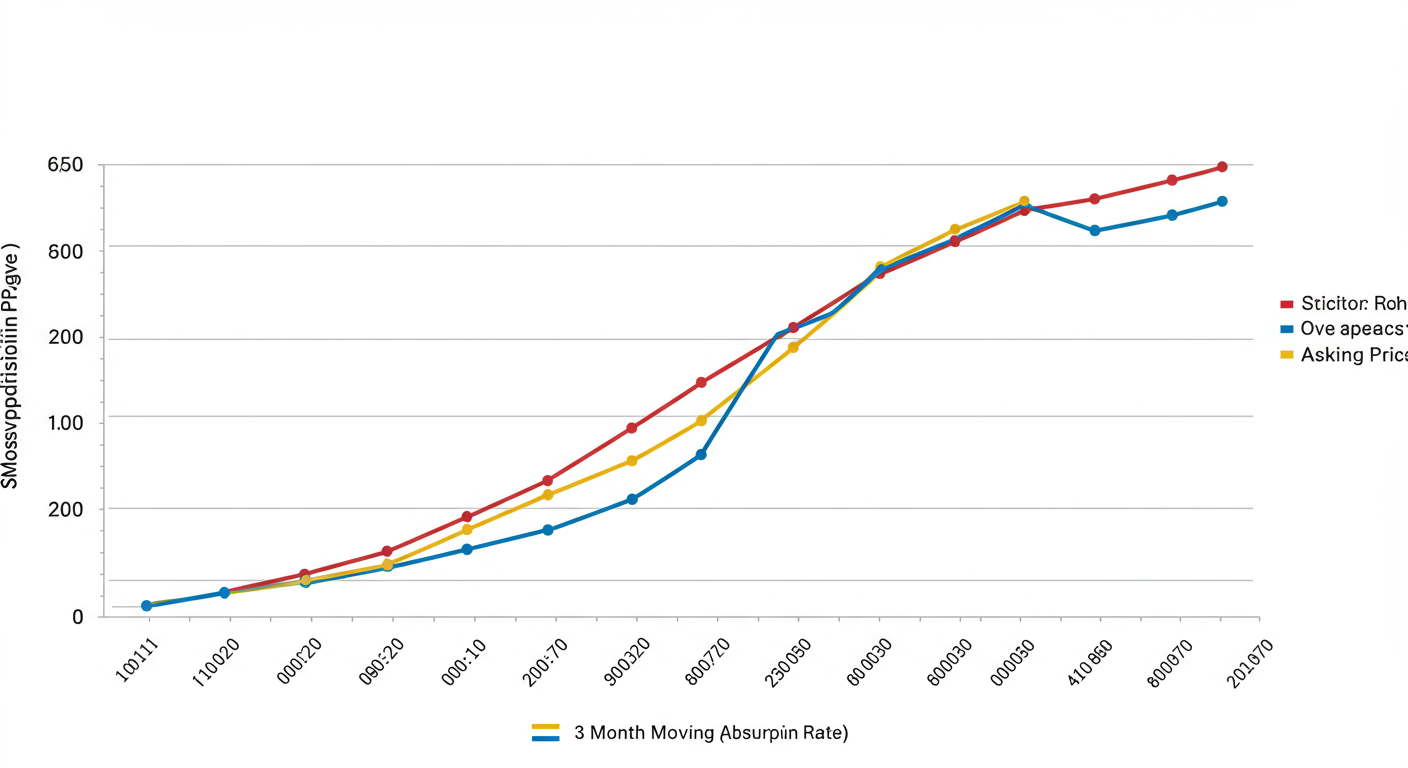

- Absorption of available inventory and the share of homes selling over the asking price improved markedly from winter lows with 36 percent of homes sold over the asking price.

- Home prices remain flat year-over-year with only Eastside, areas surrounding DTLA, South LA, and Mid City seeing an increase of 6 to 8 percent above last year.

- The home price forecast remains flat through 2020.

Detailed Analysis

Following a cheerful housing market activity for Los Angeles in April, May home sales activity slowed some, though still maintaining the momentum gained from the first quarter. Total home sales in the greater central Los Angeles area were 2 percent below last May, following April’s upwardly revised 2 percent year-over-year increase. Encouragingly, the rate of declines has slowed considerably after double-digit declines seen in the first few months of 2019 and 17 months of continual declines.

Overall, Los Angeles housing markets are experiencing an interesting dichotomy with relatively pricier West Side markets continuing to see relative weakness compared to last year and compared to some markets on the Eastern side of the city. Buyers are moderately more active in Eastern Cities (Arcadia and Monrovia), Foothill Communities (La Cañada Flintridge, La Crescenta – Montrose), East Valley (from Sherman Oaks to Glendale), and South Bay, than in Mid-City or West LA areas. The activity is largely driven by more available inventory this spring, but also search for value as much of the activity is seen with homes priced below $1 million, but also within higher price ranges.

Taking the first five months of the year together, sales are 7 percent below last year, with all price ranges trending below last year and a considerable decline in sales of homes above $2 million, which are down 14 percent year-over-year. Nevertheless, May offered some promise for homes priced between $2 million and $3 million with a 6 percent jump compared to last May. This was the first year-over-year increase following six months of double-digit declines. Sales in that price range in May reached the highest level in at least the last four years.

Sales of homes priced below $2 million posted a 2 percent decline from last year, following April’s jump of 5 percent. Even with May’s small decline, the market has seen a considerable improvement in sales compared to an extended period of year-over-year declines seen in the last year.

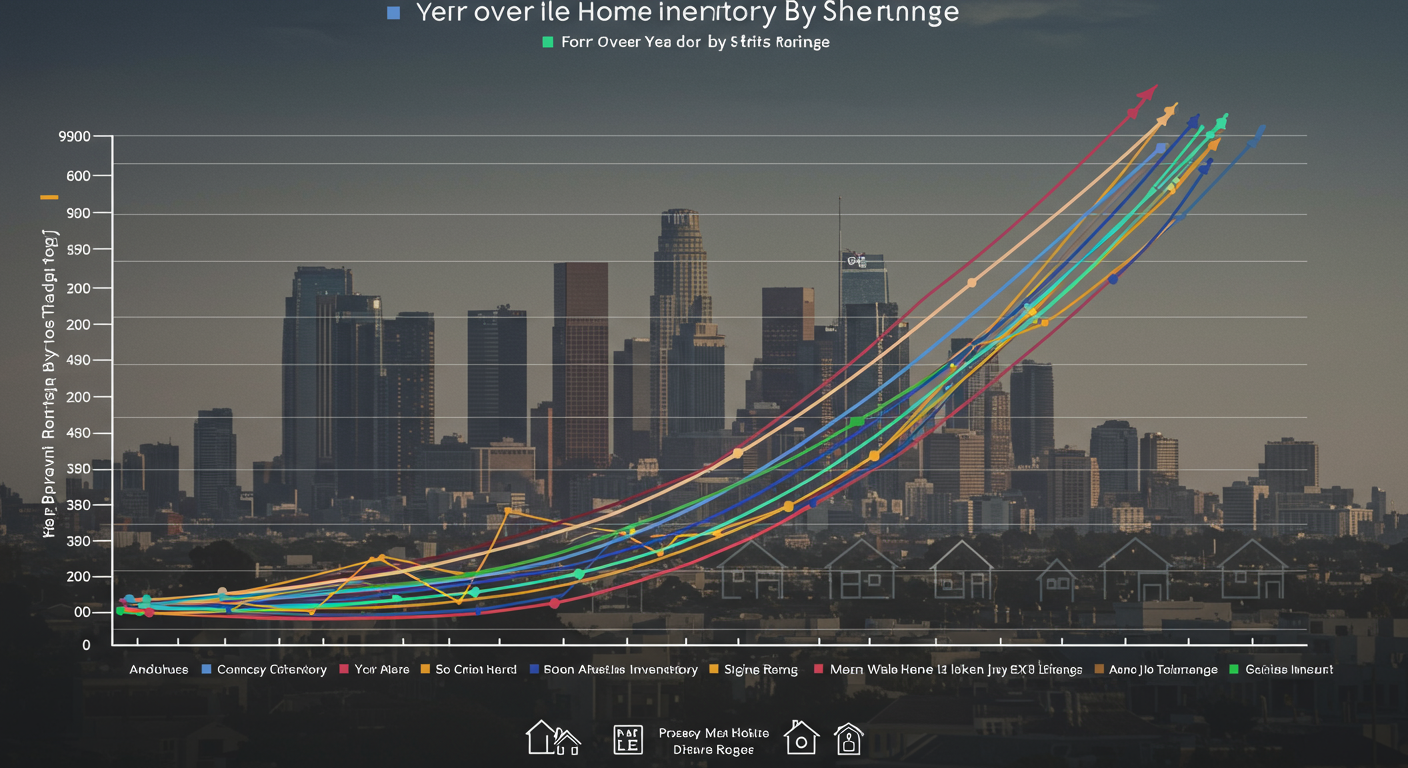

Figure 1 traces year-over-year changes in the number of homes sold by price range. While the volatility of monthly changes makes it difficult to follow the trends, note the April increases in lower price ranges, and the surge in sales between $2 million and $3 million compared to the beginning of the year.

Figure 1 Year-over-year change in the number of homes sold by price range Source: Terradatum, Inc. from data provided by local MLS, June 7, 2019

Source: Terradatum, Inc. from data provided by local MLS, June 7, 2019